Concentrated bets

When I’ve looked at all the investors (that) have very large reputations — Warren Buffett, Carl Icahn, George Soros — they all only have one thing in common. And it’s the exact opposite of what they teach in a business school. It is to make large concentrated bets where they have a lot of conviction.

Stanley Druckenmiller

| Top # stock | Holding value |

|---|---|

| Top holding | 12.1 |

| Top 3 holdings | 36.0 |

| Top 5 holdings | 55.5 |

What we do

- Bottom-up stock picking

- High conviction bets

- Investments in focused sectors

What we don’t

- Benchmark hugging

- Under-weight/overweight

- Broad-brush representation across sectors

Since inception, our portfolio’s volatility (having <15 companies) is not significantly different from our benchmark that has 500+ companies as shown below

Image Description:

The table compares the performance of the Unicorn Portfolio with the BSE S&P 500 TRI benchmark from the portfolio’s inception on March 23, 2021, through June 30, 2026. The Unicorn Portfolio, comprising 16 companies, delivered a 21.5% annualized return, outperforming the benchmark’s 13.5% return by 8 percentage points. While the portfolio experienced slightly higher volatility (17.6% vs. 14.1%) and downside risk (10.7% vs. 9.2%), it achieved stronger risk-adjusted performance, with a Sortino Ratio of 1.3 and a Sharpe Ratio of 0.7, compared with the benchmark’s 0.8 and 0.5, respectively. Overall, the Unicorn Portfolio generated higher returns while maintaining favorable risk-adjusted performance relative to the benchmark.

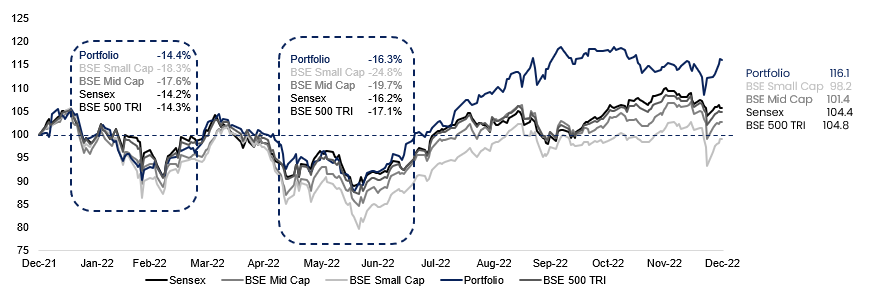

In a volatile CY2022, our drawdowns were lesser than headline indices while bounce-backs were stronger